Quick factoid reaffirms the concept of recency bias, the concept that more recent events hold greater weight than past ones, a bias we all have. In terms of human life, where and when was the deadliest wildfire since 1900? Hint, 1918 and in the US. [1]

Transferring Risk

I digress. The canary or prophet that I wish to discuss is insurance companies. They make their money by assuming a risk you would rather not take, trying as accurately as possible to predict possible losses over time and then take in sufficient funds, by themselves, boosted from investments or even reinsurance [2], to cover losses and make a profit. Most property insurers also cover casualties making it difficult to abstract the revenues from property insurance – a net margin of 4% is roughly correct, and when you have billions in premiums, that 4%, in the words of Tom Wolfe, the author of The Bonfire of the Vanities, represents “golden crumbs.”

“Catastrophe exposure”

With all these golden crumbs, why would California's #1 and #4 casualty insurance companies (State Farm and Allstate) stop issuing new home insurance? Because it is no longer possible to sustain profits – their business model is built on making bets, not on gambling. The cost of the damage inflicted by “natural disasters” is rising.

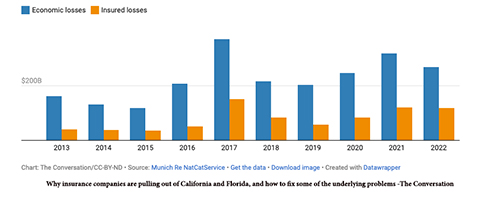

The bar graph shows the rising costs – much of this self-inflicted as we continue to live in areas where flooding, hurricanes, and forest fires are increasing.

As an article in The Conversation points out, the reinsurance cost rose 25% in 2022 and 33% in 2023; a dollar cost in 2021 is now $1.66. The decision to leave California is not predicated solely on the catastrophe exposure but may have been hastened by state law restricting the rate of rise of insurance premiums.

California is not alone. Louisiana has seen many small insurance companies, representing 16% of the market, closing or leaving the state because of hurricane damage. Florida likewise, with the added twist that fraudulent post-weather repair scams have also resulted in escalating legal costs.

In California, the FAIR plan, funded by a consortium of insurance firms, is the insurer of last resort but is meant as temporary insurance while more traditional policies are obtained. State or federal government remains the insurer of last resort – the risk is not changed by the government taking over, but the “pockets” of money used to make people “whole” is considerably deepened by the unlimited money of taxpayers.

These plans are a stop-gap and are not sustainable. We need to look at the National Flood Insurance Program of the Federal Emergency Management Agency, established in 1968. Hurricane Katrina in 2005 left the NFIP with over $20 billion in debt. As I have written previously, the decisions of the NFIP with respect to beach communities only exacerbate disparities between low and high-income individuals.

The withdrawal of insurance companies from these states with high losses due to increasingly frequent natural disasters is the silence of the coal mine’s canaries. Climate migration is already underway globally; we in the U.S. continue to ignore the canary's silence. In many instances, we are moving towards the risk. If we wish to continue as we have, we should at least adopt building and safety codes that account for climatic change.

[1] According to Statistica, it was in Cloquet, Minnesota, in 1918 and took between 400 and 1,000 lives, burning 250,000 acres. Like many wildfires, it was started by humans, or at least their railroads combined with dry conditions and wind. The acreage lost was meager compared to the largest wildfire in terms of area, which goes to the 2003 Siberian Taiga Fires in Russia, engulfing 55 million acres. The current Canadian fires are closing in on 10 million acres.

[2] Reinsurance is when an insurance company gets a larger firm to insure all or part of the risk they have taken on; AIG is a reinsurance company.

Chuck Dinerstein, MD, MBA

Director of Medicine

Dr. Charles Dinerstein, M.D., MBA, FACS is Director of Medicine at the American Council on Science and Health. He has over 25 years of experience as a vascular surgeon.