On October 15th, Medicare’s version of trick or treat opens its doors. From that date until December 7th, Medicare beneficiaries have the option and opportunity to modify their out-of-pocket costs for the next year. If you are anywhere near or over 65, it is the season of robocalls, a marked increase in the electronic and postal mail from your friends at insurance companies. And since many of us are either in that age group or have a family member in that group, I thought it was worthwhile to breakdown the choices and provide some guidance.

The basis of all plans is Medicare A and B.

Part A

This covers the cost of hospitalizations. If you have paid into Medicare through taxes on your employment for 10 years, there is no premium. If you have not paid into the system, your premium in 2019 varied between $240 and $437/month. Every time you are hospitalized, you have an out-of-pocket deductible of $1364, at least in 2019. It covers a sixty-day period from the day of initial admission. It includes skilled nursing facilities and home health care. It even covers hospital readmission during the same 60-day period. Only about 5% of individuals over age 65 are hospitalized more than once annually; for most patients, the deductible is a reasonable estimate of their actual spending.

Part B

This covers the costs of physicians, other providers, and durable medical goods. There is a monthly premium for this coverage; in 2020, it will be $144/month or $1728/annually. That premium increases for those with $170,000 in income (joint filing) for the two years before they begin Medicare. 91% of Americans, at least in 2015, had joint incomes below this level. You are also responsible for an initial out of pocket costs, a deductible of $185. You have an additional out-of-pocket expense of 20% of Medicare’s allowable charge.

Charges vary with the intensity of the visit, but at the high end, the allowable cost is $167. If your physician participates in Medicare (and most do), they will receive $133 directly from Medicare, and you will owe them the difference, in this instance, $44. If your physician does not participate in Medicare, they can bill no more than 110% of Medicare’s charge, in this instance, $183. They can require you to pay them now and need not submit your Medicare claim. If a claim is filed, you will receive 95% of the allowable charge, in this example $158, leaving you out of pocket cost at $25. This is not a bargain since you will most likely have to file the claim, a project not for the faint of heart.

Bottom Line: Without seeing any physician, your baseline cost is $1728. As you see physicians, you are responsible for the first $185. Since 94% of this age group sees a physician at least every six months, we are looking at a minimum of roughly $1913 annually.

While those current costs look negligible, it is time to take a seat. Now we have to consider the cost of drugs.

Part D

This is the part that covers the cost of your medications. It involves a monthly premium and a charge for your prescriptions. Describing the costs is, at best, a hot mess and, at worst, a project for Sisyphus. Save yourself a great deal of time and make use of Medicare’s website, Find a 2020 Medicare Plan. This website is easy to use and extremely helpful. But before using it, gather together all of your prescriptions, and they will ask you to enter them into the system. (For those with privacy concerns, you needn’t log in to run the program, but your information will be forgotten once you’re done – I would use MyMedicare.gov, which allows you to have some privacy protection and holds onto the data.

Here's a hint, the choice between generics and brand name pharmaceuticals makes a difference. Using just one relatively common brand name drug increased my out-of-pocket costs by over $3,000 annually. The website will tell you the cost of your monthly premium, your deductible, and your estimated costs for the medications. For the faint of heart, I would be sitting down, as I did these calculations.

Medigap and Medicare Advantage

There are two programs designed to help you with your Part B and D premiums and deductibles

Using the same website, you can look at both these forms of additional coverage, and to be truthful, I urge you to do so.

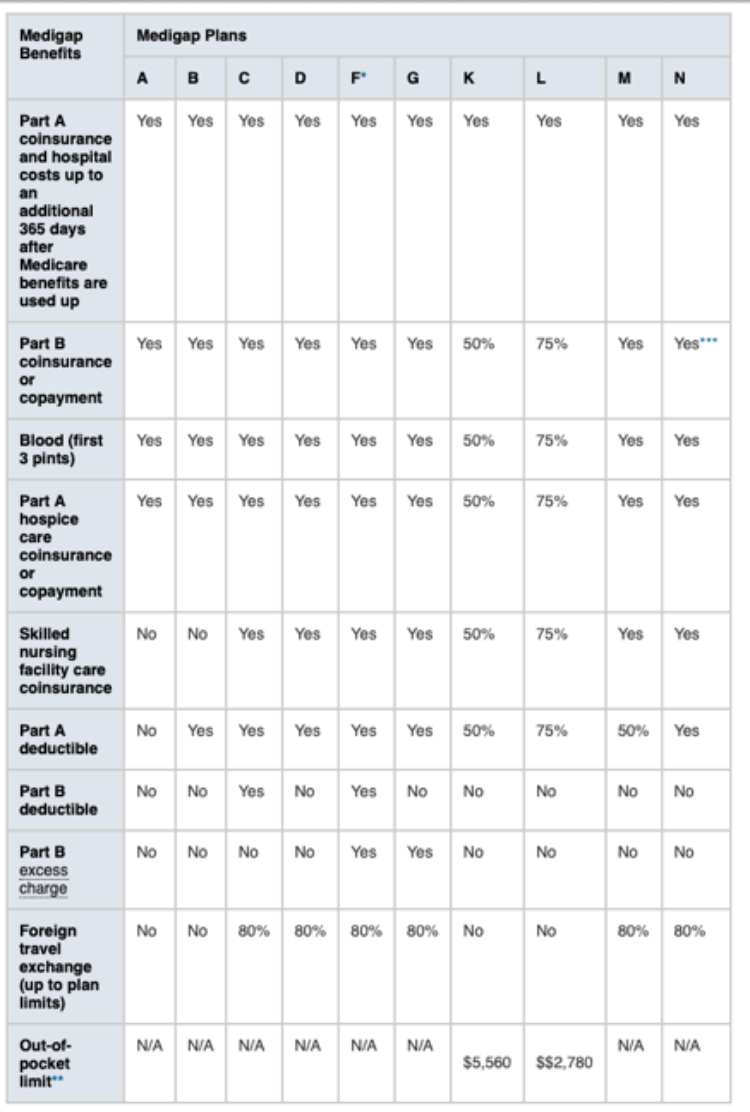

Medigap is in addition to your Part A and B costs. There are currently eleven standardized Medigap plans, although not each state offers them all. Using the websites, I have already mentioned you can determine the additional coverage they provide as well as their premiums and annual cost. The site also allows you to describe your health as excellent, good, or poor. Depending upon your description, you will see variations in your estimated out-of-pocket costs. For example, in one of the plans, my spending tripled from $5,000 to $15,000 annually based on poorer health. I have put the basics of the choices here.

Beginning in January, plan C and F will not cover the Plan B initial deductible, that means it is another $185 out of your pocket.

For those of you who just throw up your hands at all this, there is always Medicare Advantage – the one-stop-shop for healthcare insurance. About a third of Medicare beneficiaries choose this path, especially since they offer free or subsidized dental, hearing, and vision coverage. Many provide additional fitness coverage and even transportation. But you get what you pay for. These programs restrict your choice of physicians and hospitals, so the first thing to determine is whether your physicians and your closest or favorite hospital are within their network. If not, you will see your out-of-pocket costs rise. And for the travelers and snow-birds amongst us, you may find yourself in a foreign country, like Florida, paying out-of-network expenses.

Once again, have your list of drugs available and go to that Medicare website or MyMedicare.gov. Nearly all of these plans have no monthly premium, you still pay your Part B premiums, and the payments for other services vary. They will provide an estimated cost for the year.

Now is the time to look at your healthcare costs and see whether you can bring them down in the next year. I’m betting you will do better than Congress in reigning in your expenses, at least in the short term. The websites I have linked to are those of your federal government, you paid for them, they did a good job, and you should definitely use them.

Chuck Dinerstein, MD, MBA

Director of Medicine

Dr. Charles Dinerstein, M.D., MBA, FACS is Director of Medicine at the American Council on Science and Health. He has over 25 years of experience as a vascular surgeon.